SYLLABUS

GS-3: Indian Economy and issues relating to planning, mobilization of resources, growth, development and employment; Inclusive growth and issues arising from it.

Context: The Reserve Bank of India cancelled the banking licence of Paytm Payments Bank Limited, under the Banking Regulation Act, 1949, citing serious regulatory and governance failures.

More on the News

- The RBI cancelled the licence under Section 22(4), prohibiting the bank from carrying out any banking activity under Sections 5(b) and 6 of the Act with immediate effect.

- The central bank will approach the High Court for winding upof the bank; however, it has clarified that the bank has sufficient liquidity to repay all depositors.

- The action was based on multiple violations, including:

- Operations conducted in a manner detrimental to depositors’ interests (Section 22(3)(b))

- Poor management character affecting public interest (Section 22(3)(c))

- No public interest in allowing continuation (Section 22(3)(e))

- Non-compliance with licence conditions (Section 22(3)(g))

- RBI had been tightening restrictions since March 2022 (ban on new customers), followed by 2024 restrictions prohibiting deposits, credits, and wallet top-ups due to persistent compliance failures.

- The move is largely procedural culmination, with minimal impact on parent company One 97 Communications Ltd, as it had already transitioned operations to partner banks.

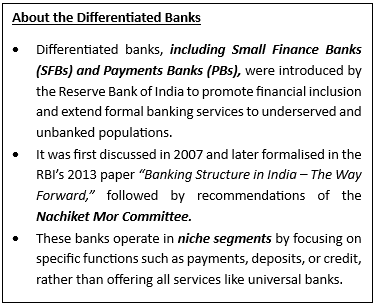

About Payments Banks

- A Payment Bank is a financial institution set up to operate on a smaller scale with minimal credit risk.

- It was introduced based on the recommendations of the Nachiket Mor Committee (2014) to promote financial inclusion by providing banking services to the unbanked and underbanked populations.

- Key Objectives:

- Serve migrant workers, low-income households, and small entrepreneurs

- Offer essential banking services such as deposits, payments, and remittances

- Facilitate the digital banking ecosystem in India

- Regulatory Framework:

- Registered under: Companies Act, 2013

- Governed by: Banking Regulation Act, 1949, RBI Act, 1934, Foreign Exchange Management Act, 1999 and Payment and Settlement Systems Act, 2007.

- Key Features of Payment Banks:

- Differentiated Banks – Unlike universal banks, they have specific operational limitations

- Smaller Scale Operations – Focus on low-value, high-volume transactions

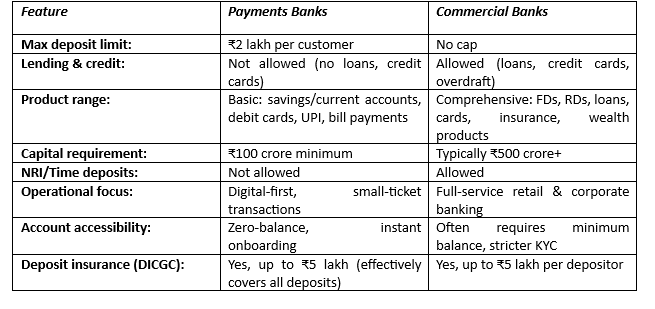

- Capital Requirements:

- Minimum paid-up capital – ₹100 crore

- Promoter’s minimum initial contribution – 40% of paid-up equity capital for the first five years

- Functions:

- Accept Deposits – Up to ₹2,00,000 per customer

- Offer Savings & Current Accounts – No time deposits allowed

- Issue Debit Cards – But no credit cards

- Invest Deposits: 75% in Statutory Liquidity Ratio (SLR) securities and 25% as time deposits with scheduled commercial banks.

- Enable personal payments and cross-border remittances

Payments Banks vs Commercial Banks