SYLLABUS

GS-3: Indian Economy and issues relating to planning, mobilization of resources, growth, development and employment.

Context: India completed nine years of the Goods and Services Tax (GST) on 1 July 2026, marking a major milestone in the country’s journey towards a unified, technology-driven, and transparent indirect tax system, further strengthened by the Next-Generation GST (GST 2.0) reforms.

About the Goods and Services Tax (GST)

- GST was enabled through the 101st Constitutional Amendment Act, 2016, which empowered both the Centre and the States to levy GST by amending the constitutional distribution of taxation powers.

- It was launched on 1 July 2017 based on the principle of “One Nation, One Tax, One Market.”

- GST is implemented through four key laws enacted in 2017—Central GST (CGST) Act, Integrated GST (IGST) Act, Union Territory GST (UTGST) Act, and GST (Compensation to States) Act.

- It replaced 17 Central and State taxes and 13 cesses, eliminating the cascading “tax-on-tax” effect and creating a common national market.

- GST is a destination-based consumption tax, levied on the supply of goods and services, with tax revenue accruing to the state where consumption occurs.

- It follows a Dual GST Model:

- CGST – Levied by the Centre on intra-state supplies.

- SGST – Levied by States on intra-state supplies.

- IGST – Levied on inter-state supplies.

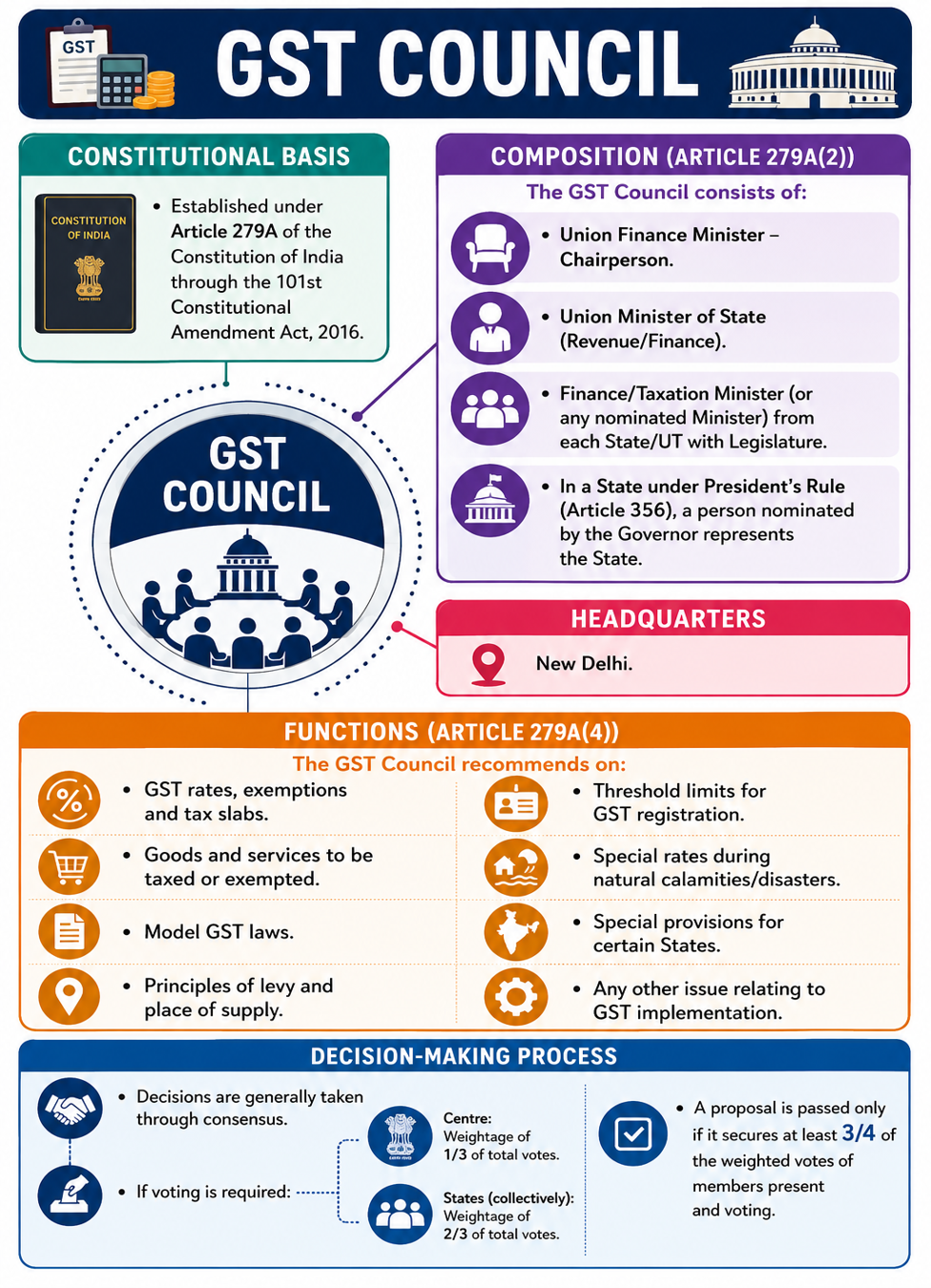

- GST Council is a constitutional body established under Article 279A that promotes co-operative federalism by enabling consensus-based decisions between the Centre and States.

- Goods and Services Tax Network (GSTN), jointly owned by the Centre and States (50:50), provides the digital backbone for registration, return filing, payments, refunds and e-invoicing.

- Coverage: GST applies to almost all goods and services, while alcohol for human consumption remains outside its ambit. Constitutionally, five petroleum products can be brought under GST on the recommendation of the GST Council.

- GST has progressively adopted AI, machine learning and data analytics to improve compliance, risk assessment, fraud detection and tax administration.

- Taxpayer base expanded from 66.5 lakh (2017) to 1.65 crore (May 2026), while gross GST collections increased from ₹7.4 lakh crore (2017-18) to ₹22.27 lakh crore (2025-26).

- Collections during April-May 2026 stood at around ₹4.37 lakh crore.

About GST 2.0 (Next-Generation GST Reforms)

- Approved in the 56th GST Council Meeting, the reforms came into effect on 22 September 2025 to simplify taxation and improve ease of doing business.

- Tax structure simplified to two principal slabs:

- 5% for essential goods and services.

- 18% for standard goods and services.

- 40% for luxury and sin goods such as tobacco, lottery/online gaming, aerated drinks, high-end cars, yachts and private aircraft.

- Compliance reforms include:

- Simpler registration and return filing.

- Faster refund processing.

- Reduced compliance costs, particularly for MSMEs and startups.

- Relief measures for MSMEs and small taxpayers:

- Registration threshold for goods suppliers increased from ₹20 lakh to ₹40 lakh.

- Composition Scheme limit enhanced from ₹75 lakh to ₹1.5 crore.

- QRMP Scheme for taxpayers with turnover up to ₹5 crore.

- NIL GST returns can be filed through SMS.

- Ease-based registration enables approval within three working days for low-risk applicants.

- Waiver of interest and penalties for specified past demand notices (FY 2017-18 to FY 2019-20), subject to conditions.

- Technology-driven administration has been strengthened through:

- E-invoicing.

- Pre-filled returns.

- Automated Input Tax Credit (ITC) matching.

- AI-enabled risk-based scrutiny and compliance monitoring.

Significance

- Creates a unified national market by replacing multiple indirect taxes with a single integrated tax framework.

- Promotes co-operative federalism through consensus-based decision-making in the GST Council.

- Improves ease of doing business by simplifying tax rates, reducing compliance burden and accelerating refunds, especially for MSMEs and startups.

- Enhances transparency and tax compliance through digital platforms, e-invoicing, AI-based analytics and real-time validation.

- Supports formalisation of the economy, reflected in a significant rise in registered taxpayers and sustained growth in GST revenues.

- Reduces production costs through rationalised tax rates and correction of inverted duty structures, improving domestic manufacturing and export competitiveness.

- Benefits consumers by lowering prices on several goods and services, increasing affordability and improving access to essential sectors such as healthcare.

- Contributes to macroeconomic stability by strengthening revenue buoyancy, fiscal transparency and data-driven tax administration while supporting the vision of Viksit Bharat.