SYLLABUS

GS-2: Bilateral, regional and global groupings and agreements involving India and/or affecting India’s interests.

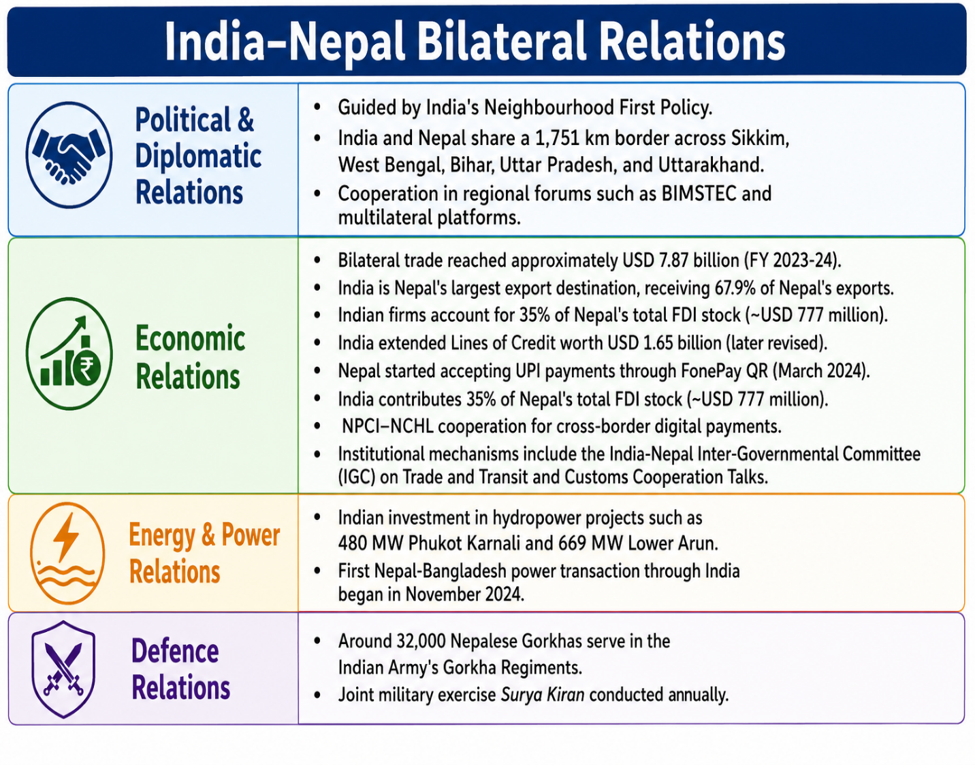

Context: In a major boost to digital financial connectivity and neighbourhood cooperation, India and Nepal officially launched a peer-to-peer (P2P) cross-border remittance mechanism.

About the Peer-to-Peer (P2P) Cross-Border Remittance Mechanism

- The mechanism establishes a direct linkage between India’s Unified Payments Interface (UPI) and Nepal’s National Payments Interface (NPI).

- It enables citizens of both countries to make seamless, real-time, secure, and instant money transfers across borders through mobile banking applications and digital wallets.

- The system allows individuals to transfer funds directly without relying on traditional banking channels or carrying physical cash.

- The technical integration was implemented through collaboration between NPCI International Payments Limited (NIPL), the international arm of the National Payments Corporation of India (NPCI), and Nepal Clearing House Limited (NCHL).

- The initiative forms part of broader regional efforts to promote safe, accessible, and affordable cross-border payment systems.

Significance of the Mechanism

- Strengthens Financial Inclusion: Expands access to fast and secure digital financial services for citizens of both countries.

- Enhances India–Nepal Economic Ties: Deepens digital and economic integration while reinforcing longstanding social and people-to-people connections.

- Facilitates Real-Time Cross-Border Transfers: Enables instant remittances and reduces dependence on slower conventional banking channels.

- Improves Traveller Convenience: Eliminates the need for physical currency exchange, carrying large amounts of cash, and dealing with unfamiliar payment systems.

- Supports Local Businesses and Merchants: Provides Nepalese merchants greater access to Indian visitors, potentially increasing transaction volumes and digital payments.

- Boosts Operational Efficiency: Enables optimized cash management, lowers cash-handling costs, and ensures secure real-time settlement of transactions.

- Promotes Regional Digital Connectivity: Advances the goal of creating interoperable digital payment ecosystems in South Asia.

- Expands UPI’s Global Footprint: The linkage further strengthens UPI’s international presence.

- UPI is currently accepted in nine countries—Singapore, the United Arab Emirates, France, Mauritius, Nepal, Bhutan, Qatar, Sri Lanka, and Cambodia.