SYLLABUS

GS-3: Indian Economy and issues relating to Planning, Mobilization of Resources, Growth, Development and Employment; Effects of Liberalization on the Economy, Changes in Industrial Policy and their Effects on Industrial Growth.

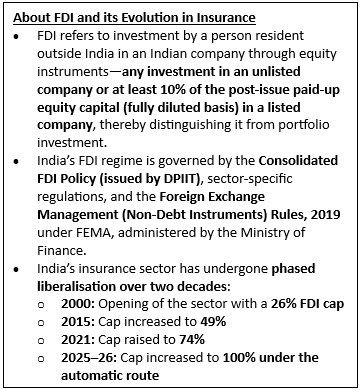

Context: The Government of India has notified 100% Foreign Direct Investment (FDI) in the insurance sector under the automatic route by amending the Foreign Exchange Management (Non-debt Instruments) Rules, 2019.

More in the News

- The reform has been operationalised through the Foreign Exchange Management (Non-Debt Instruments) (Second Amendment) Rules, 2026, in line with the Sabka Bima Sabki Raksha (Amendment of Insurance Laws) Act, 2025, which raised the FDI cap from 74% to 100% under the automatic route.

- This marks a significant step in the liberalisation of the sector, aimed at enhancing capital availability, improving insurance penetration, and strengthening India’s financial ecosystem.

Key Highlights of the Reform

- Automatic Route for 100% FDI: Foreign investors can now invest up to 100% in insurance companies and intermediaries via the automatic route, simplifying entry and reducing regulatory delays.

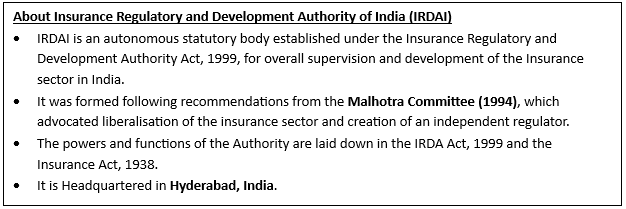

- Regulatory Oversight and Safeguards: Investments remain subject to IRDAI regulations, solvency norms, and governance requirements, ensuring financial stability and policyholder protection.

- Applicability to Intermediaries: The reform extends beyond insurers to include insurance intermediaries, broadening the scope of foreign participation in the ecosystem.

- Special Provision for LIC: The amendment retains a differentiated cap for the Life Insurance Corporation of India (LIC), where FDI remains capped at 20% under the automatic route.

Significance of 100% FDI in Insurance

- Capital Inflows and Sector Deepening: The reform is expected to attract stable, long-term global capital, strengthening the financial base of insurers and expanding market depth in an under-penetrated sector.

- Competition and Innovation: Entry of foreign players can bring advanced product design, data-driven underwriting, and digital distribution models, enhancing efficiency and consumer experience.

- Improved Insurance Penetration: Increased investment and competition can help expand coverage in health, crop, and micro-insurance, supporting broader social protection goals.

- Boost to Financial Ecosystem: The reform supports financial inclusion, risk management, and long-term savings mobilisation, contributing to overall economic stability.

Challenges and Concerns

- Regulatory and Supervisory Challenges: Full foreign ownership necessitates enhanced regulatory vigilance by IRDAI and other financial regulators, particularly in areas such as solvency, pricing, and cross-border risk management.

- Consumer Protection Risks: The proliferation of complex insurance products and digital sales channels may lead to information asymmetry and mis-selling, especially in rural and low-literacy markets.

- Impact on Domestic Players: Increased competition may put pressure on public sector insurers and smaller domestic firms, requiring them to improve efficiency and innovation.

- Profit Repatriation and Strategic Concerns: Greater foreign ownership may lead to higher profit repatriation and raise concerns about control over a strategically important financial sector.

Way Forward

- Strengthening Regulatory Oversight: Strengthen regulatory capacity and oversight mechanisms to ensure financial stability and effective consumer protection.

- Ensuring a Level Playing Field: Promote a level playing field between domestic and foreign players while encouraging innovation and healthy competition.

- Enhancing Consumer Awareness and Transparency: Enhance financial literacy and transparency to safeguard consumer interests and prevent mis-selling.

- Expanding Inclusive Insurance Coverage: Encourage inclusive insurance expansion, particularly in underserved and rural areas, to improve penetration and social protection.