SYLLABUS

GS-2: Welfare schemes for vulnerable sections of the population by the Centre and States and the performance of these schemes.

GS-3: Inclusive growth and issues arising from it.

Context: The Atal Pension Yojana (APY), a flagship social security initiative of the Government of India administered by the Pension Fund Regulatory and Development Authority (PFRDA), has achieved a significant milestone by crossing 9 crore gross enrolments as of April 2026.

More on the News:

- This reflects the expanding reach of pension coverage among India’s unorganised workforce and marks a major step toward universal social security.

- The scheme has witnessed steady and impressive growth since its launch:

- Total enrolments crossed 9 crore subscribers (April 2026).

- FY 2025–26 recorded over 1.35 crore new enrolments, the highest ever in a single financial year.

About Atal Pension Yojana (APY)

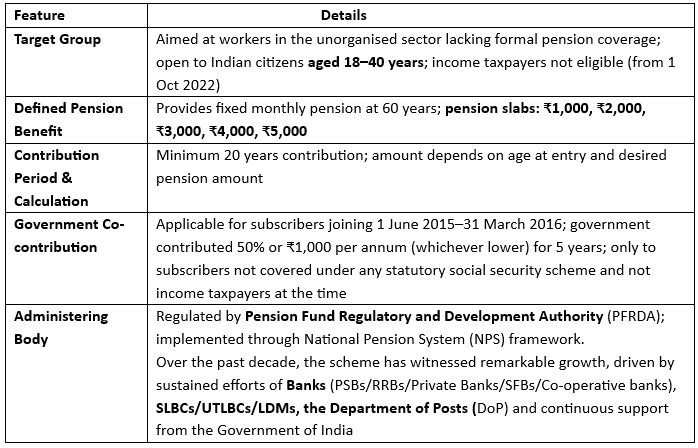

- APY, launched by the Government of India on 9 May 2015 and operational from 1 June 2015.

- The scheme was designed to encourage voluntary savings for retirement by offering defined pension benefits, linked to the age of joining and amount of contribution.

- Targeted primarily at poor and underprivileged workers in the informal sector, the scheme has emerged as one of the most inclusive and accessible social security initiatives in India.

Background and Rationale

- A majority of India’s workforce operates outside formal employment structures, lacking access to structured retirement benefits.

- This creates:

- Dependence on family support in old age

- Financial insecurity after working years

- Absence of a stable savings mechanism

- APY was introduced as a response to these structural gaps, aiming to create a sustainable and inclusive pension framework.

Salient Features of APY

Benefits and Social Security Impact

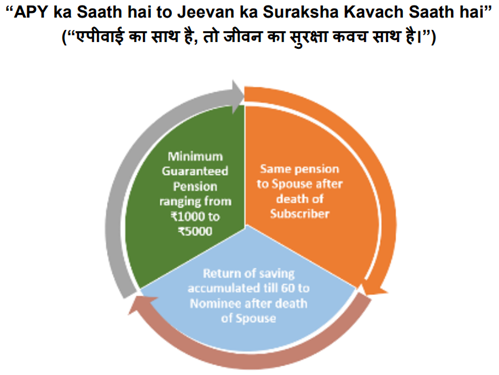

- Assured Pension: Lifelong fixed pension ensures income stability after retirement

- Family Protection: Spouse receives pension after subscriber’s death; nominee receives accumulated corpus

- Auto-Debit Facility: Ensures regular and disciplined savings

- Tax Benefits: Contributions eligible under relevant provisions of the Income Tax Act

Exit and Withdrawal Provisions

- The scheme promotes long-term savings discipline: Pension benefits begin at the age of 60

- Premature exit is allowed only under exceptional conditions like death or terminal illness

- Voluntary exit leads to return of contributions with interest, excluding government contribution

Challenges

- Economic Constraints

- Limited ability of low-income groups to contribute regularly

- Pension amounts may remain modest in the long term

- Social Constraints

- Low awareness and financial literacy in informal sectors

- Irregular income affecting continuity of contributions

- Administrative Challenges

- Ensuring deeper penetration in rural and remote areas

- Sustaining long-term participation across decades

Implications

- For Individuals

- Provides financial independence during old age

- Reduces vulnerability and dependency

- For Economy

- Encourages long-term savings

- Strengthens financial inclusion

- For Society

- Supports social security for vulnerable populations

- Reduces pressure on informal family-based support systems

Institutional Efforts and Awareness Measures

- Awareness campaigns at state and district levels

- Training and outreach programmes

- Use of digital platforms such as e-APY, mobile apps, and online banking

- Multilingual information dissemination

- Help desks, chatbots, and QR-based services for subscriber support

Way Forward

- Short-Term Measures

- Strengthen awareness campaigns and outreach

- Simplify onboarding and contribution mechanisms

- Long-Term Measures

- Enhance pension adequacy over time

- Improve financial literacy and digital inclusion

- Institutional Strengthening

- Strengthen coordination between financial institutions and regulators

- Expand digital and multilingual service delivery