SYLLABUS

GS-3: Achievements of Indians in science & technology; indigenization of technology and developing new technology; Awareness in the fields of IT.

Context: NITI Aayog has released India’s first comprehensive 10-year roadmap, ” Future of India’s Semiconductor Industry”, aimed at building a USD 120–150 billion semiconductor value chain by 2035 and positioning India as an indispensable player in the global semiconductor ecosystem.

Key Highlights of the Roadmap

• Why India Must Act Now:

- Nearly 90–95% of India’s semiconductor demand is met through imports.

- Dependence on imported chips poses strategic risks to defence, aerospace and critical infrastructure systems.

- India spent nearly USD 150 billion on semiconductor imports during FY17–FY25, resulting in significant foreign exchange outflows.

- Domestic semiconductor production is essential for making future technologies such as 5G/6G devices more affordable and accessible.

- Global supply-chain diversification and the China-plus-One strategy have created a narrow but critical window of opportunity for India to enter the semiconductor value chain.

• India’s Semiconductor Opportunity:

- The global semiconductor market is expected to exceed USD 1.5 trillion by 2035.

- India’s semiconductor demand is projected to reach around USD 200 billion by 2035.

- At present, nearly 90–95% of India’s semiconductor demand is met through imports.

- Global supply-chain realignments and the search for trusted manufacturing destinations provide India with a historic opportunity to strengthen its position in the value chain.

• Vision 2035: Becoming Indispensable, Not Imitative

- India aims to capture 10–13% of the global semiconductor market by 2035.

- The roadmap seeks to retain 55–70% of semiconductor value capture within India through local design, packaging, materials and manufacturing ecosystems.

- The roadmap targets the creation of a USD 120–150 billion semiconductor value chain by 2035.

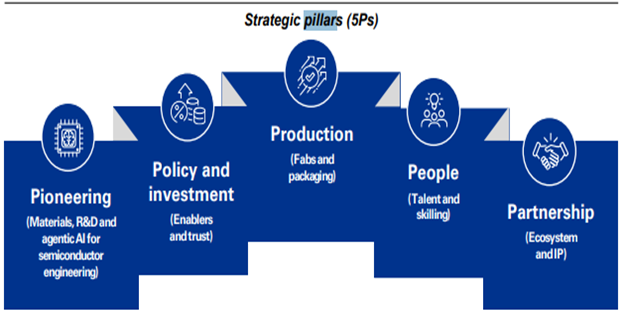

• The strategy is based on three pillars:

1. Strategic self-sufficiency.

2. Ecosystem strength.

3. Global indispensability.

- The emphasis is on building leadership in areas where India possesses structural advantages rather than competing directly in every segment of the semiconductor industry.

- India aims to achieve 15–25% chip self-sufficiency by 2030.

- Self-sufficiency is expected to increase to 35–50% by 2035.

• Leadership in Advanced Packaging and OSAT:

- India aims to emerge as one of the top three global destinations for advanced packaging and OSAT (Outsourced Semiconductor Assembly and Testing).

- Focus areas include Chiplets, 2.5D and 3D integration, Fan-Out Wafer Level Packaging (FOWLP), Panel-Level Packaging (PLP) and System-in-Package (SiP) technologies.

- Advanced packaging is identified as a major opportunity in the emerging “More-than-Moore” era.

• Focus on Compound and Wide-Bandgap Semiconductors:

- The roadmap prioritises leadership in Silicon Carbide (SiC) and Gallium Nitride (GaN) technologies.

- India aims to become a major supplier of wide-bandgap semiconductor materials.

- These technologies are critical for electric vehicles, renewable energy systems, power electronics, telecom infrastructure and defence applications.

• Strengthening Semiconductor Design Capabilities:

- Tiered subsidies for Electronic Design Automation (EDA) tools are proposed to reduce design costs and improve access for startups and researchers.

- An AI-enabled Semiconductor Engineering Mission is proposed to shorten chip-design cycles through agentic AI tools and automation.

- The roadmap targets the creation of more than 100 advanced semiconductor design IPs by 2035.

- Priority areas include AI-native chip design, high-performance computing, quantum computing, system architecture and chiplet-based design.

- The objective is to move from a design-services hub to a creator of globally competitive semiconductor IP.

• Building Domestic Manufacturing Capacity:

- Wafer fabrication efforts will primarily focus on mature logic nodes between 28 nm and 65 nm.

- Special emphasis is placed on analog, mixed-signal and power-management chips used in automotive, IoT and industrial applications.

- The roadmap recommends exploring Small Modular Reactors (SMRs) to provide reliable dedicated power for semiconductor fabrication clusters.

• Alignment with India Semiconductor Mission (ISM) 2.0:

- The roadmap complements the objectives of India Semiconductor Mission (ISM) 2.0 announced in Union Budget 2026.

- It marks India’s transition from ecosystem creation to ecosystem deepening.

- Greater emphasis is placed on design, manufacturing, packaging, materials, talent development, research and innovation and global partnerships.

• Major Challenges Identified:

- Rising technological complexity is making semiconductor design and manufacturing increasingly difficult.

- India faces shortages of specialised talent required for fabrication, packaging and advanced research.

- Semiconductor manufacturing requires high capital investments, energy resources and water availability.

- Building trust and acceptance for India-made chips within global supply chains will require sustained efforts.

- Long gestation periods and slow returns increase the financial risks associated with semiconductor investments.

• Roadmap’s Key Solutions:

- Establish a National Frontier Semiconductor Research Programme to accelerate frontier semiconductor R&D.

- Create a National Design and Packaging Co-Design Platform to strengthen indigenous design capabilities.

- Develop a National Fab Academy to build a semiconductor-ready workforce.

- Establish a National Semiconductor Capital Framework to mobilise long-term investments.

- Build sovereign capabilities in semiconductor design, research and advanced packaging.

- Develop a robust domestic manufacturing ecosystem focused on strategic and high-value segments.

- Create a complete semiconductor talent pyramid from technicians to solution architects.

- Mobilise long-term capital through government support and private-sector participation.

- Strengthen trusted international partnerships to accelerate technology acquisition and ecosystem growth.