SYLLABUS

GS-3: Indian Economy and issues relating to Planning, Mobilization of Resources.

Context: Public Sector Banks (PSBs) have registered strong financial performance during FY 2025–26, reflecting sustained business growth, improved asset quality, record profitability and strong capital position.

Key Highlights of the Financial Performance

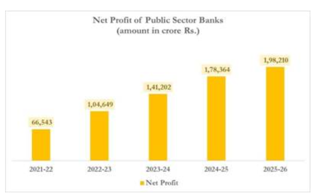

- PSBs recorded their highest-ever aggregate net profit of ₹1.98 lakh crore in FY 2025-26, registering an annual growth of 11.1%, marking the fourth consecutive year of aggregate profitability for PSBs.

- The aggregate business of PSBs increased to ₹283.3 lakh crore, registering growth of 12.8% over the previous year.

- Aggregate deposits rose by 10.6% to ₹156.3 lakh crore, while gross advances increased by 15.7% to ₹127 lakh crore.

- Credit growth remained broad-based across major sectors:

- Retail advances increased by 18.1%.

- Agriculture advances grew by 15.5%.

- MSME advances expanded by 18.2%.

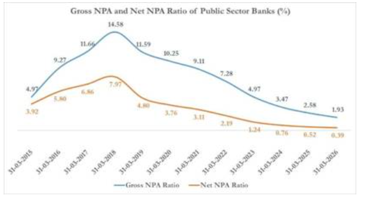

- Asset quality of PSBs also improved significantly:

- Gross NPA ratio (Non-Performing Assets) declined to 1.93%.

- Net NPA (NNPA) ratio fell to 0.39%, the lowest-ever level for PSBs.

- Slippage ratio declined to 0.7%.

- Aggregate Capital to Risk-Weighted Assets Ratio (CRAR) improved to 16.6%, well above regulatory requirements of 11.5%.

- PSBs reported recoveries worth nearly ₹86,971 crore, including recoveries from written-off accounts.

Factors Behind the Turnaround of PSBs

- Government-Led Banking Reforms:

- The 4R Strategy — Recognition, Resolution, Recapitalisation, and Reforms — helped address legacy stressed assets and improve banking discipline.

- The Government launched the Mission Indradhanush programme in 2015 to improve appointments, governance, capitalisation, accountability, and autonomy in PSBs.

- RBI’s Regulatory and Supervisory Measures:

- The RBI’s Asset Quality Review (AQR), initiated in 2015, ensured transparent recognition of stressed assets and prevented evergreening of loans.

- Implementation of Basel III norms strengthened capital adequacy, risk management, and prudential regulation within PSBs.

- The Prompt Corrective Action (PCA) framework imposed operational discipline on weak banks and improved financial prudence.

- Strengthening Recovery and Resolution Mechanisms:

- The enactment of the Insolvency and Bankruptcy Code (IBC), 2016, significantly improved recovery mechanisms and credit discipline among borrowers.

- Establishment of the National Asset Reconstruction Company Limited (NARCL) facilitated the resolution of large stressed assets.

Significance for the Indian Economy

- Enhancing Financial Stability: Stronger PSBs improve systemic stability and reduce the fiscal burden associated with repeated bank recapitalisation.

- Supporting Economic Growth: Improved balance sheets enable PSBs to expand credit flow towards infrastructure, manufacturing, MSMEs, agriculture, and priority sectors.

- Deepening Financial Inclusion: PSBs continue to play a central role in implementing Jan Dhan Yojana, Direct Benefit Transfers (DBT), rural banking expansion, and social security schemes.

- Strengthening Investor and Depositor Confidence: Sustained profitability, lower NPAs, and stronger capital adequacy enhance confidence in India’s banking and financial ecosystem.