SYLLABUS

GS 3:Indian Economy and issues relating to planning, mobilisation of resources, growth, development and employment and Infrastructure: Energy, Ports, Roads, Airports, Railways, etc.

Context: Recently, the fifth edition of the ‘Trade Watch Quarterly’ for Quarter I of the financial year (FY) 2025–26 (April–June 2025) was released in New Delhi by NITI Aayog.

More on the News:

- The report presents a data-driven analysis of India’s trade performance amid evolving global conditions.

- The publication highlights emerging structural shifts in India’s trade profile, including the rising contribution of technology-intensive exports, the continued strength of services-led growth, and changes in import composition reflecting deeper integration into global value chains.

- The thematic section of this quarter’s edition focuses on India’s automotive exports, examining India’s export footprint across vehicles and auto components.

- The first edition was released on December 4, 2024, and analyses India’s trade statistics for Q1 FY24 (April to June 2024), providing a snapshot of India’s trade position, sectoral performance, and emerging opportunities.

Major Highlights of the Report

- India’s Trade Analysis (Q1 FY26):

- India’s total trade (merchandise + services) was up 3.7% y-o-y, with services trade up 7% and merchandise trade up 2% making total trade as $439 bn.

- Merchandise Trade: Exports declined by 2.1% y-o-y to $112 bn, and imports rose marginally by ~5% reaching $180 bn.

- Exports of electrical machinery surged, while those of mineral fuels declined, primarily due to reduced petroleum exports to the Netherlands, the US and the UAE.

- Increase in imports was driven by growth in inorganic chemicals, electrical machinery and nuclear reactors.

- Services Trade: Exportswitnessed a robust annual expansion of 10%, reaching $97 bn, and services imports rose marginally by 1.56% to $49.5 bn during the same period, resulting in a net services trade surplus of $48 bn.

- The combined balance of trade in goods and services registered a net deficit of $21 bn for this quarter.

- Regional Contribution: India’s exports to its top markets, including the USA, UAE, the Netherlands, China and the UK, remained steady.

- Exports increased to the USA, China, and Germany, but declined to the UK and the Netherlands, partly due to lower petroleum exports.

- India’s share of imports from its top markets – China, UAE, Russia, USA increased, though declined with Iraq, Russia and Saudi Arabia.

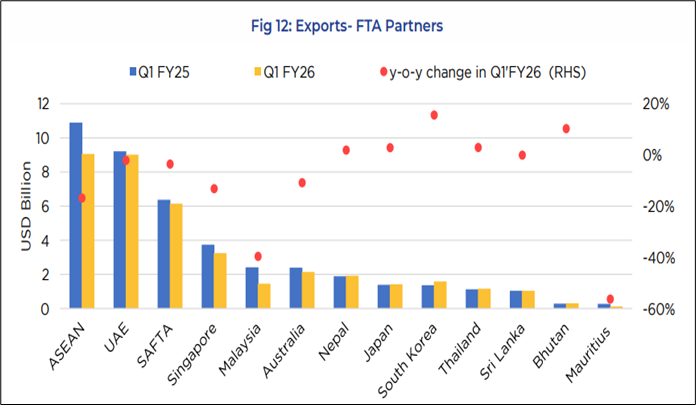

- Trade with FTA partners: India’s trade performance with its Free Trade Agreement (FTA) partner countries in Q1 FY26 reflected a widening trade deficit.

- Sectoral Contribution: Technology-intensive sectors, electronics, machinery, and chemicals, now anchor India’s trade performance.

- Electronics emerged as the standout performer, contributing to over 11% of total exports, reflecting deeper integration into global electronics supply chains.

- Creative Economy: India ranks modestly in creative goods exports ($20.6bn) dominated by software and R&D, but performs far more strongly in creative services ($94.2bn), ranking fourth globally

- This contrast highlights India’s core strength in skill-intensive, digital, and innovation-driven creative activities, thus well-positioning itself in the rapidly evolving global creative economy.

- Thematic analysis: Automotive exports

- India’s automobile exports expanded from $9.4 bn to $13.2 bn, registering a compound annual growth rate of 3.5%.In contrast, exports of auto components grew much faster, nearly doubling from $8.2 bn to $16.9 bn.

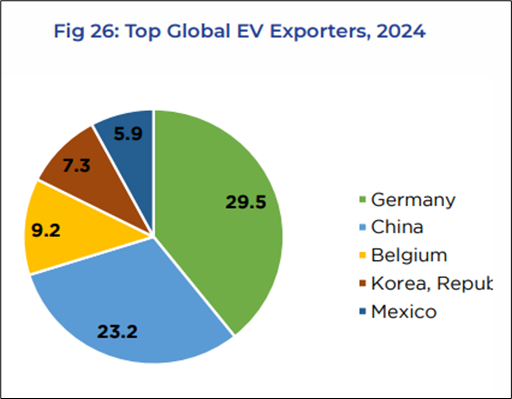

- Technology transition: India’s Electric Vehicle (EV) exports increased from $1.2 mn in 2020 to $84 mn in 2024, showing high growth but still accounting for about 0.1% of global exports ($145 bn).

- Export destination: India mainly sells small and affordable EV to Nepal (46.4%) Indonesia (20.9%) and Japan (20.1%).

- Import market: Germany remains the top source, largely due to high-end car imports, while China’s share is also increasing.

- Key Issues: India exports low-value vehicles but imports high-spec models and key components, limiting its competitiveness and long-term role in the global EV value chain.

Key Recommendations of the Report

- Enhance export competitiveness: The report emphasises rationalising incentives, expanding export-linked financing for emerging markets, and accelerating domestic production of critical inputs such as EV batteries to enhance export competitiveness.

- Strategic Engagement with Key Markets: India’s export push needs to be recalibrated toward neighbouring and emerging markets such as Sri Lanka, Africa, and Latin America, where significant untapped demand persists.

- Strengthening Quality Standards: Reviving the Indian Brand Equity Foundation (IBEF) can play a central role in improving India’s global branding, quality standards through “Made in India” as a credible and competitive label.

- Addressing Non-Tariff Barriers: Enhance government-to-government engagement to streamline regulatory compliance and reduce market-specific NTBs.