SYLLABUS

GS 3: Indian Economy and issues relating to Planning, Mobilization of Resources, Growth, Development and Employment.

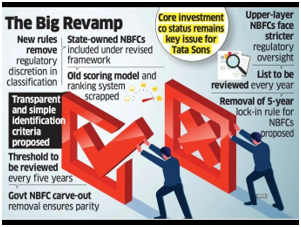

Context: The Reserve Bank of India has issued draft Amendment Directions to revise the methodology for identifying NBFC-Upper Layer (NBFC-UL) entities under the Scale-Based Regulatory (SBR) Framework and to include Government-owned NBFCs in this category.

Background:

• The Scale-Based Regulatory (SBR) Framework identifies NBFC-Upper Layer (NBFC-UL) using two methods: top 10 eligible NBFCs by asset size and a parametric scoring methodology.

• Government-owned NBFCs are currently placed only in the Base Layer or Middle Layer and are not considered for the Upper Layer.

Objective and Proposed Changes:

• Asset Size-Based Classification: To ensure a transparent, simple, and objective system, it is proposed to replace the existing methodology with a single asset size criterion of ₹1,00,000 crore and above.

- This threshold will be reviewed every five years.

• Removal of Automatic Top 10 Rule:

- Discontinues automatic inclusion of top 10 NBFCs

- Moves away from ranking-based identification

• Inclusion of Government-Owned NBFCs: To promote an ownership-neutral regulatory regime, eligible Government-owned NBFCs are proposed to be included in the NBFC-UL category based on the revised criteria.

• Additionally, all NBFC-UL entities are proposed to be allowed to use State Government guarantees as credit risk transfer instruments without any limit, subject to specified conditions.

Scale Based Regulation Framework for NBFC:

| Layer | Category | Criteria |

| Base Layer (NBFC-BL) | Low-risk NBFCs | Non-deposit NBFC with asset size below ₹1000 crore; NBFC Peer-to-Peer; NBFC Account Aggregator |

| Middle Layer (NBFC-ML) | Moderate-risk NBFCs | Deposit-taking NBFC (irrespective of size); NBFCs with asset size of ₹1000 crore and above; Standalone Primary Dealer; Infrastructure Debt Fund NBFCs |

| Upper Layer (NBFC-UL) | High-risk / systemically important NBFCs | NBFCs identified by RBI based on parameters and scoring methodology; eligible NBFCs based on asset size irrespective of other factors |

| Top Layer (NBFC-TL) | Extreme risk (empty by default) | Ideally remains empty; includes NBFCs from Upper Layer with substantial increase in systemic risk as identified by RBI |

Implications of the New Approach:

• Regulatory clarity:

- Removes ambiguity of scoring-based classification

- Provides clear compliance threshold for large NBFCs

• Impact on large conglomerates:

- Large holding companies like Tata Sons may fall under NBFC-UL based on asset size

- This increases regulatory oversight and compliance requirements

• Listing debate relevance:

- The revised framework may further clarify the regulatory position, especially for core investment companies

Key Challenges:

• Increased regulatory burden may raise compliance costs due to stricter norms for more NBFCs entering the upper layer.

• Asset-based classification may overlook risk diversity and qualitative factors like interconnectedness.

• Inclusion of government NBFCs may reduce operational flexibility and increase compliance pressure.

• Ownership and governance issues (e.g., Tata Sons case) may create regulatory and restructuring challenges.

Significance of the Proposal

• Simplification of regulatory framework through clear asset-based criteria

• Enhances transparency and predictability in classification

• Moves towards uniform treatment of public and private NBFCs

• Strengthens systemic risk monitoring for large NBFCs

• May expand the number of NBFCs classified under the Upper Layer