Syllabus:

GS-3: Indian Economy and issues relating to planning, mobilization of resources, growth, development and employment; Inclusive growth and issues arising from it.

Context:

Recently, the Prime Minister marked the 11 transformative years of the Pradhan Mantri Jan Dhan Yojana (PMJDY).

Pradhan Mantri Jan Dhan Yojana (PMJDY)

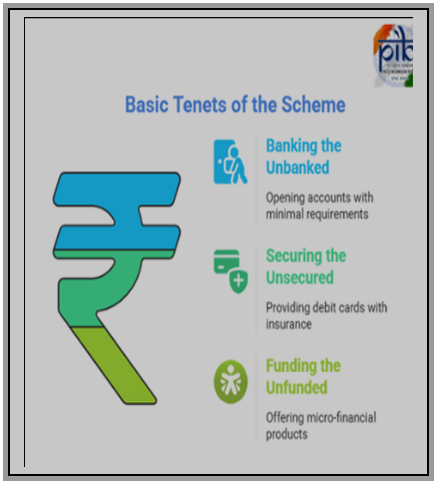

- PMJDY is one of the world’s largest financial inclusion initiatives, launched on August 28, 2014.

- It is a National Mission on Financial Inclusion, which has an integrated approach to bring about comprehensive financial inclusion and provide banking services to all households in the country.

- Scheme envisages universal access to banking facilities with at least one basic banking account for every household, financial literacy, access to credit, insurance and pension facility.

- Eligibility: PMJDY applicants must be Indian nationals aged 18–59 years, while minors above 10 can open accounts with guardian support.

Benefits under PMJDY

- Basic Savings Bank Deposit Account: It provides a basic savings account for the unbanked with zero minimum balance, interest on deposits and a RuPay Debit card is provided to the account holder.

- Accident Insurance Cover: All beneficiaries receive an accident insurance cover of ₹2 lakh.

- Overdraft facility up to ₹10,000 is available to one account per household, with an additional ₹5,000 loan after six months of satisfactory account activity.

- Eligibility for Additional Government Schemes: PMJDY accounts are eligible for Direct Benefit Transfer and government schemes such as MUDRA loans, Atal Pension yojana etc.

Achievements of the PMJDY

- Deposits in Account: Over 56.16 crore bank accounts have been opened under the PMJDY, with total deposits reaching ₹2.67 lakh crore as of mid-August 2025,

- Rural Penetration: 67% of the accounts belong to rural or semi-urban areas with the active involvement of Business Correspondents (BCs) / Bank Mitras.

- Women at the Forefront of PMJDY: 56% Jan Dhan accounts belong to women, highlighting the scheme’s role in promoting gender equality in financial access and financial empowerment of women, particularly in the unorganised sector.

- Broadening Financial Horizons: It serves as the foundation for Direct Benefit Transfer in over 300 schemes, reducing leakages and middlemen.

- Number of RuPay Debit Cards Issued: 38.68 crore RuPay debit cards have been issued to PMJDY account holders, enabling cashless transactions and accident insurance access.

- The JAM Trinity: The Jan-Dhan-Aadhaar-Mobile (JAM) trinity, with PMJDY at its core, has proven to be a diversion-proof mechanism for subsidy delivery with ₹6.9 lakh crore credited to bank accounts under DBT schemes in FY 2024–25.

Concerns of the Scheme

- High Zero Balance Accounts: RBI data showed nearly 23% of Jan Dhan accounts had zero balance, although the share has declined over the years.

- Inoperative Accounts: As of July 30, 2025, 13.05 crore (130.5 million) PMJDY accounts are inoperative or dormant, out of a total of 56.04 crore accounts opened under the scheme.

- Hidden charges: Private Banks levy hidden charges on the beneficiary, which may become a deterrent for financial inclusion.

- Overdraft Facility: Overdraft facility is discretionary with the concerned banks. Many banks may decline to extend the overdraft facility, therefore defeating the purpose.

- Low Financial Literacy: The lack of awareness among beneficiaries about PMJDY-linked insurance and pension schemes weakens its empowerment potential.

Way Forward

- Reduce Dormancy: Promote account activity by linking transactions with PMJDY and raising beneficiary awareness on regular usage benefits.

- Transparent Banking Practices: Strictly monitor banks to prevent hidden charges and ensure zero-cost services for beneficiaries.

- Strengthen Financial Literacy: Launch targeted awareness drives on insurance, pensions, and credit facilities to empower beneficiaries.

- Streamline Overdraft Facility: Standardise and simplify overdraft eligibility criteria across banks to ensure uniform access.