SYLLABUS

GS-2: Welfare schemes for vulnerable sections of the population by the Centre and States and the performance of these schemes.

Context:

Recently, the government has introduced a one-time, one-way switch for central government employees who initially opted for the Unified Pension Scheme (UPS), allowing them to revert to the National Pension System (NPS).

More on the News

- As per the Finance Ministry, the Central government employees who initially chose the Unified Pension Scheme (UPS) now have a one-time option to switch back to the National Pension System (NPS).

- The initiative aims to provide an informed choice to Central Government employees in planning their post-retirement financial security

Key Provisions of the Switch

• The Department of Financial Services has allowed the switch under the following conditions:

- Eligible employees under UPS can switch to NPS only once, and cannot switch back to UPS.

- The switch must be exercised at least one year before superannuation or three months before voluntary retirement, whichever is applicable.

- The switch facility will not be allowed in case of removal, dismissal or compulsory retirement as a penalty or in cases where disciplinary proceedings are ongoing or contemplated.

- Those who do not opt for the switch within the stipulated time will continue under UPS by default.

- Employees who choose to remain in NPS cannot opt for UPS after 30th September 2025.

Understanding the Schemes

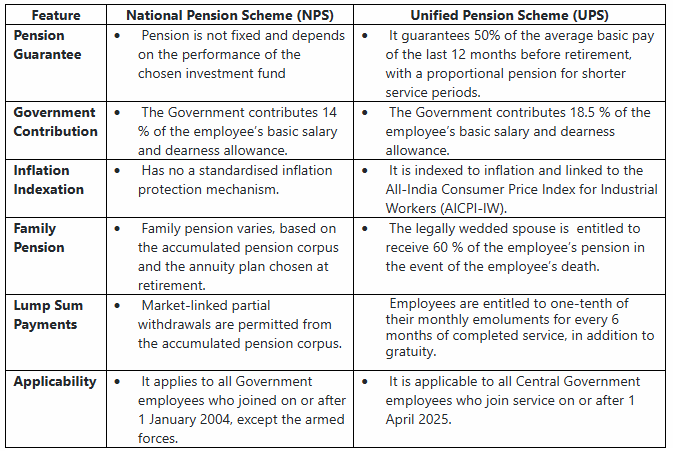

Unified Pension Scheme (UPS)

- UPS was introduced as an option under NPS for central government staff covered under NPS so that they may receive an assured payout after their retirement.

- It is a ‘fund-based’ payout system which relies on the regular and timely accumulation and investment of applicable contributions from both the employee and the employer (the Central Government) for grant of monthly payout to the retiree.

- Assured pension: 50% of the average basic pay drawn over the last 12 months prior to retirement for a minimum qualifying service of 25 years. This pay is to be proportionate for lesser service period up to a minimum of 10 years of service.

- Assured Minimum Pension: Minimum assured pension of ₹10,000 per month for employees completing at least 10 years of qualifying service, subject to regular contributions and no withdrawals.

- Assured Family Pension: 60% of the employee’s pension, shall be provided to the legally wedded spouse immediately after demise.

- Inflation Indexation: Under UPS, pension is linked to Dearness Allowance (DA), ensuring inflation protection.

- Lump Sum Payment: 10% of monthly emoluments (basic pay + Dearness Allowance) for every completed six months of qualifying service will be allowed.

- Dearness Relief: It is based on All India Consumer Price Index for Industrial Workers (AICPI-IW) as in the case of service employees

- Risk Free: Low-risk and government-backed, offering stability and security.

National Pension System (NPS)

- NPS is a market-linked defined contribution scheme introduced by the Central Government to help the individuals receive income in the form of pension for their retirement needs.

- Diversification: Investments diversified across equities, corporate bonds, and government securities.

- Pension Option: Allows withdrawal of 60% of the accumulated corpus as a lump sum at retirement; the remaining 40% must be used to purchase an annuity.

- Voluntary Model: The voluntary model is available to all the citizens of India including those residing abroad, between the age of 18 and 70 years.

- Portable: Each employee is identified by a separate Permanent Retirement Account Number (PRAN) which is portable and remains the same even if an employee gets transferred to any other office.

- Tax Benefit: Provides tax benefits under Sections 80C and 80CCD of the Income Tax Act.

- Growth Option: Offers higher growth potential through market-linked returns.

Comparison of National Pension Scheme (NPS) and Unified Pension Scheme (UPS)