Context:

The Financial Action Task Force (FATF) is working towards adopting new norms for higher disclosures by financial institutions, for cross-border payments.

Key Highlights:

- FATF are discussing stricter rules for cross-border credit card transactions and if they are adopted by the FATF then Indian regulators will have to implement those rules.

- FATF is working towards new norms for higher disclosures by financial institutions, payment aggregators, and fintech companies for cross-border payments.

- An International consultative forum will be held in Mumbai in April 2025 through the FATF platform to discuss the above issue with participants from the Indian industry, private sector, and regulators of other member countries.

- The FATF is also looking to revise its Recommendation 16, under which the beneficiary financial institution is supposed to verify the identity of the beneficiary for qualified wire transfers.

- The FATF had placed India in the “regular follow-up” category (need to submit a follow up report once in three years on a voluntary basis). It is a distinction shared by only four other G20 countries including the United Kingdom, France and Italy.

What is the need for new disclosure?

- The new set of norms aids to investigation agencies with “real-time information” about senders and receivers of funds via these channels.

- The intention behind these norms is to enhance transparency and facilitate the identification of fund senders and receivers, which is crucial in combating money laundering, terrorist financing, and proliferation financing.

Impact of Higher Disclosure by FATF

- Costs for credit card companies, payment aggregators and fintech firms are likely to go up as the global Financial Action Task Force (FATF) is planning to increase disclosure requirements, mainly for cross-border transactions.

- The payment industry is concerned that the new requirements could lead to investment in software and other infrastructure that would result in higher costs of compliance.

India’s opinion

- The higher disclosure norms have to be formulated in such a manner that there is a balance between compliance and the industry’s concerns.

- The Indian government says it won’t adopt stricter norms at the cost of ease of doing business.

Financial Action Task Force (FATF)

- FATF was founded in 1989 on the initiative of G7 for leading global action to tackle money laundering. Later, in 2001 terrorist and proliferation financing was also added to its mandate.

- The FATF also works to stop funding for weapons of mass destruction.

- India joined with ‘observer’ status in 2006 and became a full member of FATF in 2010.

Headquarters: Paris, France.

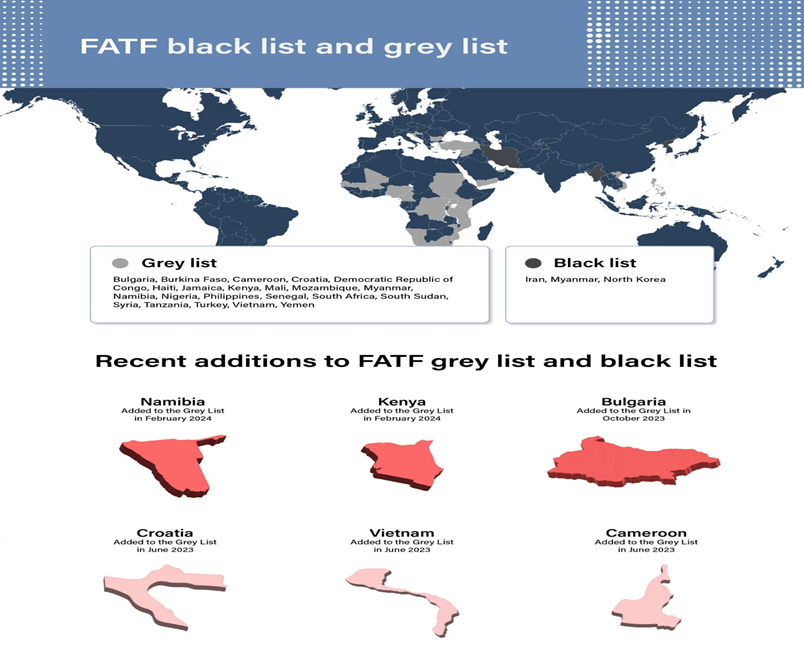

- Black List: If countries identify with serious strategic deficiencies to counter money laundering, terrorist financing, and financing of proliferation. This list is often externally referred to as the blacklist.

- Currently, 3 countries under the blacklist: Iran North Korea and Myanmar.

- Grey list: It identifies countries that are actively working with the FATF to address strategic deficiencies in their regimes to counter money laundering, terrorist financing, and proliferation financing.