SYLLABUS

GS-3: Indian Economy and issues relating to Planning, Mobilization of Resources, Growth, Development and Employment.

Context: Recently, the Union Finance Minister Nirmala Sitharaman tabled the Economic Survey 2025-26 in both the Lok Sabha and Rajya Sabha, ahead of the Union Budget 2026.

More on the News

- The Economic Survey 2025–26 is an annual report prepared by the Chief Economic Adviser and presents the Government of India’s official assessment of the country’s economic performance, structural challenges, and policy priorities in FY 2025–26.

Key Highlights of the Economic Survey

STATE OF THE ECONOMY

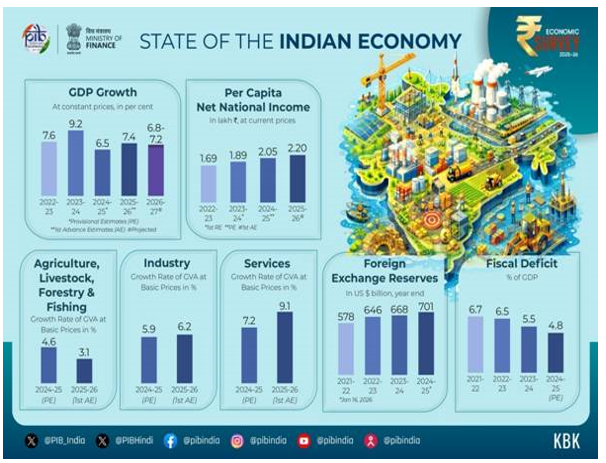

- The First Advance Estimates place FY26 real GDP growth at 7.4 per cent and GVA growth at 7.3%, reaffirming India’s status as the fastest-growing major economy for the fourth consecutive year.

- Private Final Consumption Expenditure grew by 7.0 per cent in FY26, reaching 61.5 per cent of GDP, the highest since 2012 (FY23 also recorded 61.5 per cent share).

- Gross Fixed Capital Formation is growing by 7.8%, and its share remains steady at 30% of GDP.

- Gross Value Added (GVA) for services in the first half of FY26 increased by 9.3 per cent, with an estimated 9.1 per cent growth for the entire fiscal year.

FISCAL DEVELOPMENTS: ANCHORING STABILITY THROUGH CREDIBLE CONSOLIDATION

- Centre’s Revenue Receipts strengthened from an average of about 8.5 per cent of GDP in FY16–FY20 to 9.2% of GDP in FY25 (PA).

- Income tax returns filed are increasing from 6.9 crore in FY22 to 9.2 crore in FY25.

- Gross GST collections during April–December 2025 stood at ₹17.4 lakh crore, registering a year-on-year growth of 6.7 per cent.

- Effective capital expenditure of the Central government rose from an average of 2.7 per cent of GDP in the pre-pandemic period to about 3.9 per cent post-pandemic, and to a higher 4 per cent of GDP in FY25.

- Through Special Assistance to States for Capital Expenditure (SASCI), the Centre has incentivised States to maintain capital spending at around 2.4 per cent of GDP in FY25.

- The combined fiscal deficit of State Governments stayed broadly stable at around 2.8 per cent of GDP in the post-pandemic period, similar to pre-pandemic levels, but has edged up in recent years to 3.2 per cent in FY25, reflecting emerging pressures on State finances.

- India reduced its general government debt-to-GDP ratio by about 7.1 percentage points since 2020.

MONETARY MANAGEMENT AND FINANCIAL INTERMEDIATION: REFINING THE REGULATORY TOUCH

- GNPA ratio standing at 2.2% in September 2025 and net NPA ratio at 0.5% in September 2025, reached a multi-decadal low level and record low level, respectively.

- As of 31 December 2025, the year-on-year growth in outstanding credit by scheduled commercial banks (SCBs) increased to 14.5 per cent compared to 11.2 per cent in December 2024.

- The Pradhan Mantri Jan Dhan Yojana (PMJDY), launched in 2014, has opened 55.02 crore accounts as of March 2025, with 36.63 crore in rural and semi-urban areas.

- During FY26 (till December 2025), 235 lakh of Demat accounts were added, pushing the total count beyond 21.6 crore. A key milestone was the crossing of the 12-crore mark for unique investors in September 2025, with nearly a fourth of them being women.

EXTERNAL SECTOR: PLAYING THE LONG GAME

- Between CY 2005 & CY 2024, India’s share of global merchandise exports nearly doubled from 1 per cent to 1.8 per cent, while its share of global commercial services exports more than doubled from 2 per cent to 4.3 per cent.

- India’s total exports reached a record USD 825.3 billion in FY25, registering a 6.1 per cent year-on-year growth.

- Non-petroleum exports reached a historic high of USD 374.3 billion in FY25, while non-petroleum, non-gems and jewellery exports constituted nearly four-fifths of aggregate merchandise exports.

- Services exports touched an all-time high of USD 387.6 billion in FY25, growing by 13.6 per cent.

- India’s current account deficit remained moderate at around 1.3 per cent of GDP in Q2 FY26.

- India remained the world’s largest recipient of remittances, with inflows reaching USD 135.4 billion in FY25.

- India’s foreign exchange reserves increased to USD 701.4 billion as of 16 January 2026, providing import cover of about 11 months and covering over 94 per cent of external debt.

- India continued to attract substantial foreign direct investment, with gross FDI inflows reaching USD 64.7 billion during April-November 2025.

- India ranked fourth globally in Greenfield investment announcements in 2024, with over 1,000 projects and emerged as the largest destination for Greenfield digital investments between 2020-24.

INFLATION: TAMED AND ANCHORED

- Average headline retail inflation in India moderated sharply to 1.7% in FY26 (April–December) from 6.7% in FY23.

- Food inflation declined steadily during FY26 and entered deflationary territory from June 2025.

- Global headline inflation declined from a peak of 8.7% in CY 2022 to 4.2% in CY 2025.

AGRICULTURE AND FOOD MANAGEMENT

- The agriculture and allied sector recorded an average annual growth of around 4.4% over the last five years at constant prices.

- Between FY15 and FY24, the livestock sector’s GVA increased by nearly 195%, growing at a CAGR of 12.77% at current prices.

- In FY 2024–25, foodgrains output is estimated at 3,577.3 lakh metric tonnes, an increase of 254.3 LMT over the previous year.

SERVICES: FROM STABILITY TO NEW FRONTIERS

- Services’ share in GDP rose to 53.6 per cent in H1 FY26; Services’ share in GVA stood at the highest ever – 56.4 per cent – as per FAE of FY26.

- The services sector continues to be the largest recipient of foreign direct investment inflows, accounting for an average of 80.2 per cent of total FDI during FY23-FY25, up from 77.7 per cent in the pre-pandemic period (FY16-FY20).

INDUSTRY’S NEXT LEAP: STRUCTURAL TRANSFORMATION AND GLOBAL INTEGRATION

- Industrial activity strengthened in FY26, with Industry GVA growing 7.0% (real terms) in H1.

- Manufacturing growth accelerated, with GVA expanding 7.72% in Q1 and 9.13% in Q2 FY26, reflecting structural recovery.

- India’s innovation performance has strengthened steadily, with its Global Innovation Index rank improving to 38th in 2025 from 66th in 2019.

INVESTMENT AND INFRASTRUCTURE: STRENGTHENING CONNECTIVITY, CAPACITY AND COMPETITIVENESS

- The Government of India’s capital expenditure has increased nearly 4.2 times, from ₹2.63 lakhcrore in FY18 to ₹11.21 lakh crore in FY26 (BE), while effective capital expenditure in FY26 (BE) is ₹15.48 lakh crore.

- National highway infrastructure expanded substantially, with the NH network growing by about 60 per cent from 91,287 km (FY14) to 1,46,572 km (FY26, up to December), and operational High-Speed Corridors increasing nearly ten-fold—from 550 km (FY14) to 5,364 km (FY26, up to December)

- Railway infrastructure continued to expand, with the rail network reaching 69,439 route km as of March 2025, a targeted addition of 3,500 km in FY26, and 99.1 per cent electrification achieved by October 2025.

- India has emerged as the world’s third-largest domestic aviation market, with the number of airports increasing from 74 in 2014 to 164 in 2025.

- The power sector recorded sustained capacity expansion, with installed capacity rising 11.6 per cent (y-o-y) to 509.74 GW as of November 2025, and the demand–supply gap declined from 4.2 per cent in FY14 to nil by November 2025

- Tele-density reached 86.76 per cent, and 5G services are now available in 99.9 per cent of districts in the country.

- Space infrastructure strengthened, with India becoming the fourth nation to achieve autonomous satellite docking (SpaDeX), alongside expanded indigenous missions and increased private-sector participation.

ENVIRONMENT AND CLIMATE CHANGE: BUILDING A RESILIENT, COMPETITIVE AND DEVELOPMENT-DRIVEN INDIA

- During 2025-26 (up to 31st December 2025), a total of 38.61 GW of renewable energy capacity has been installed in the country, which includes 30.16 GW of solar power, 4.47 GW of wind power, 0.03 GW of Bio-Power and 3.24 GW of hydro power.

EDUCATION AND HEALTH: WHAT WORKS AND WHAT’S NEXT

- India today operates one of the world’s largest school systems, serving 24.69 crore students across 14.71 lakh schools, supported by over 1.01 crore teachers (UDISE+ 2024-25).

- Since 1990, India has reduced its maternal mortality rate (MMR) by 86 per cent, far exceeding the global average of 48 per cent. A 78 per cent decline in the under-five mortality rate (U5MR) was achieved, surpassing the global reduction of 61 per cent and a 70 per cent decline in the neonatal mortality rate (NMR) compared to 54 per cent globally during 1990-2023.

- The infant mortality rate (IMR) marked a drop of more than 37 per cent over the past decade, declining from 40 deaths per thousand live births in 2013 to 25 in 2023.

EMPLOYMENT AND SKILL DEVELOPMENT: GETTING SKILLING RIGHT

- A total of 56.2 crore people (aged 15 years and above) were employed in Q2 FY26, reflecting a creation of around 8.7 lakh new jobs in Q2 compared to Q1 of FY26.

- The Labour Codes have formally recognised gig and platform workers, expanding social security, welfare funds, and benefit portability.

- The National Scheme for Upgradation of ITIs proposes to upgrade 1,000 government ITIs, including 200 hub ITIs and 800 spoke ITIs, through smart classrooms, modern labs, digital content, and industry-aligned long- and short-term courses.

RURAL DEVELOPMENT AND SOCIAL PROGRESS: FROM PARTICIPATION TO PARTNERSHIPS

- According to the revised World Bank’s poverty line, India’s poverty rates in 2022-23 were 5.3 per cent for extreme poverty and 23.9 per cent for lower-middle-income poverty.

- The general government’s social services expenditure (SSE) stands at 7.9% of GDP in FY 2025-26 (BE) against 7.7% in 2024-25 (RE) and 7% in 2023-24.

FROM IMPORT SUBSTITUTION TO STRATEGIC RESILIENCE AND STRATEGIC INDISPENSABILITY

- ‘Swadeshi’ must be a disciplined strategy, as not all import substitution is either feasible or desirable. A disciplined approach to indigenisation is presented through a three-tiered framework that distinguishes critical vulnerabilities with high strategic urgency, economically feasible capabilities with strategic payoffs, and low strategic urgency or high-cost substitution.

- A National Input Cost Reduction Strategy that treats competitiveness as infrastructure, recognising affordable and reliable inputs.

- A progression from ‘Swadeshi’ to Strategic Resilience to Strategic Indispensability, in which intelligent import substitution invests in national strength and ultimately embeds India in global systems, so that the world moves from “thinking about buying Indian” to “buying Indian without thinking”.