Current context:

Recently, a report published by finance ministry has predicted India’s GDP growth rate likely to be 7%.

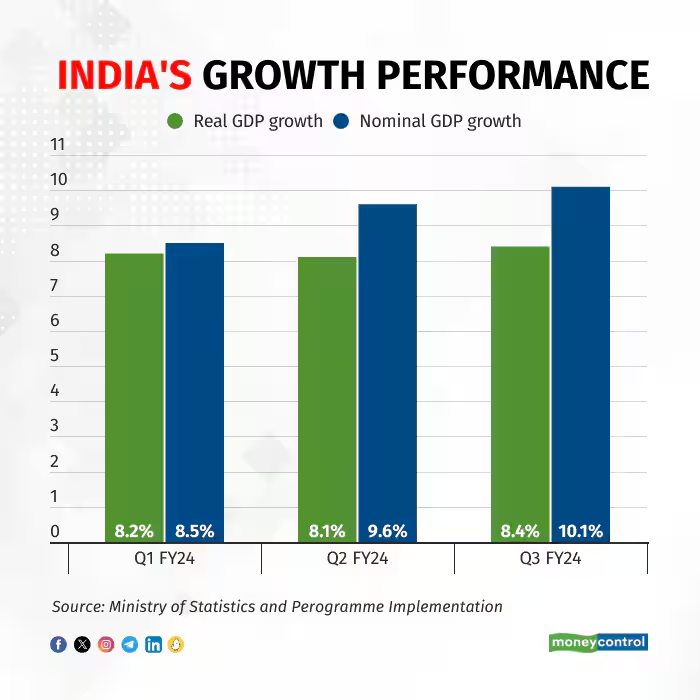

About current context:

- According to report India’s GDP growth rate for the second quarter of FY24 stands at an impressive 7.6 percent.

- This growth has exceeded earlier projections by the Reserve Bank of India (RBI), which had estimated a 6.5 percent growth rate for the same period.

- Notably, India’s growth rate surpasses that of major economies like Russia, the USA, China, and the UK during this time.

- The manufacturing and construction sectors experienced significant growth, with exports contributing to GDP from 21.4% in Q1 to 21.9% in Q2.

- Government incentives have benefited sectors like mobile phone and electronics manufacturing, but trade, transport, hotels, and communications have experienced a slowdown.

- As of December 2023, India’s current GDP is approximately $3.73 trillion1. This robust economic performance reflects India’s resilience and potential on the global stage.

India’s GDP growth faces several challenges.

- Inflation: India is grappling with inflation, which can negatively impact citizens’ purchasing power and potentially hinder economic growth.

- Unemployment: High unemployment rates pose a significant challenge, necessitating the creation and provision of employment opportunities for the expanding workforce.

- Fiscal Deficits: Managing fiscal deficits (the gap between government revenue and expenditure) is critical. Overspending can strain the economy.

- COVID-19 Impact: The COVID-19 pandemic has significantly disrupted economic activities, affecting production, consumption, and investment.

- Structural Issues: The growth of a business is hindered by bureaucratic red tape and inadequate infrastructure, necessitating the need for process streamlining and investment in infrastructure.

To enhance India’s robust GDP growth rate, several strategic steps can be taken:

- Investment in Infrastructure: Strengthening infrastructure, including transportation, energy, and digital connectivity, is crucial. This will boost productivity and attract private investment.

- Skill Development: Focusing on skill development programs ensures a competent workforce. Upskilling and reskilling initiatives can align skills with industry demands.

- Ease of Doing Business: Simplifying regulations, reducing bureaucracy, and improving the ease of doing business will encourage entrepreneurship and attract foreign investment.

- Agricultural Reforms: Modernizing agriculture, improving supply chains, and promoting agri-tech can enhance productivity and rural income.

- Manufacturing Sector: Encouraging domestic manufacturing through incentives, R&D support, and export promotion will create jobs and boost economic growth.

- Financial Sector Reforms: Strengthening the banking system, enhancing credit availability, and promoting financial inclusion are essential.

- Environmental Sustainability: Balancing growth with environmental conservation is critical. Sustainable practices can lead to long-term benefits.

- Export Diversification: Expanding export markets beyond traditional sectors diversifies the economy and reduces dependence on specific industries.

- Innovation and Research: Investing in research, development, and innovation fosters technological advancements and competitiveness.

- Social Sector Investments: Improving healthcare, education, and social safety nets ensures inclusive growth.