SYLLABUS

GS-3:Indian Economy and issues relating to planning, mobilisation of resources, growth, development and employment.

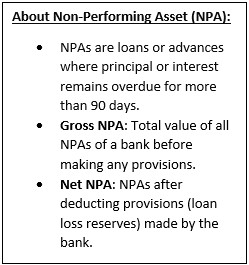

Context: India’s banking sector recorded a sharp improvement in asset quality as gross non-performing assets declined to a multi-decade low by September 2025.

More on the News

- The Reserve Bank of India released a Report on Trend and Progress of Banking in India 2024-25, highlighting sustained improvement in the asset quality of scheduled commercial banks.

- The report assessed trends in gross and net NPAs recovery performance, slippages and restructuring during 2024–25.

- It showed that better recoveries and account upgrades played a major role in reducing stressed assets.

Key Findings on Asset Quality

- Gross NPA ratio: Declined to 2.1 per cent at the end of September 2025 from 2.2 per cent in March 2025.

- Gross NPAs in absolute terms fell to ₹4.32 lakh crore in 2024–25 from ₹4.81 lakh crore in 2023–24.

- Net NPA ratio: remained stable at 0.5 per cent during the same period.

- The improvement in asset quality has continued consistently since 2018–19.

Bank-wise Trends

- Public sector banks reduced their GNPA ratio to 2.6 per cent from 3.5 per cent.

- Private sector banks recorded a marginal improvement with GNPA falling to 1.8 per cent.

- Foreign banks improved their asset quality with GNPA declining to 0.9 per cent.

- Small finance banks witnessed deterioration in asset quality with GNPA rising to 3.6 per cent.

Role of Recoveries and Upgrades

- Nearly 42.8 per cent of the reduction in GNPAs during 2024–25 was due to recoveries and upgrades.

- Banks recovered bad loans worth ₹67,693 crore.

- Stressed accounts worth ₹50,087 crore were upgraded to standard assets.

Slippages and Standard Assets

- The slippage ratio declined for the fifth consecutive year to 1.4 per cent at the end of March 2025.

- The slippage ratio in banking is a key metric that measures the rate at which a bank’s good (standard) loans are turning into non-performing assets (NPAs) within a specific period.

- By September 2025, the slippage ratio further improved to 1.3 per cent.

- The share of standard assets in total advances rose to 97.7 per cent for scheduled commercial banks.

Restructured Advances

- The ratio of restructured standard advances declined for both overall and large borrowal accounts.

- Public sector banks led the reduction in restructured advances.

- Private sector banks continued to have a lower share of restructured standard advances than public sector banks.

Significance of the Report

- Reinforces Confidence in Financial Stability: The sustained decline in bad loans demonstrates that India’s banking system is structurally stronger, enhancing confidence among investors, depositors and global rating agencies.

- Creates Headroom for Sustainable Credit Expansion: Improved asset quality and strong capital buffers enable banks to expand lending without compromising prudential norms, supporting long-term economic growth.

- Validates Effectiveness of Regulatory Interventions: The report reflects the success of RBI’s past supervisory actions on stressed assets and retail credit, indicating improved risk management across banks.

- Signals Institutional Readiness for Emerging Risks: By integrating climate risk assessment into financial oversight, the report shows that India’s banking regulator is preparing the system for future systemic and transition risks.

Source:

Indian Express

Reuters