Syllabus

GS 3: Issues related to direct and indirect farm subsidies and minimum support prices of agriculture products

Context:

Recently, China’s unpredictable export restriction has caused Supply chain disruption of di-ammonium phosphate (DAP) in India.

More on the News

- This has led to Di-Ammonia Phosphate (DAP) prices rising to almost $800 per tonne in June, the highest in the last few months.

- High DAP prices could jeopardise the Indian government’s subsidy maths for FY26 and hurt the margins of companies importing such fertilisers (subsidies cover a significant part of DAP prices).

- India’s DAP stock at the start of this year’s Kharif season (June 1) was only 12.4 lakh tonnes which is much lower than 21.6 lakh tonnes last year and 33.2 lakh tonnes two years ago.

- China has intermittently imposed restrictions on fertiliser exports —including specialty fertilisers —primarily by delaying or withholding CIQ (China’s Entry-Exit Inspection and Quarantine) clearance.

About DAP

- Composition: Contains 18% nitrogen (N) and 46% phosphorus (P₂O₅)

- Form: Dry, granular fertiliser

- Solubility: Highly soluble in water, quickly available to plants

- DAP is an important fertiliser that provides phosphorus (P), which crops need for early root and shoot growth.

- Farmers typically apply it during sowing, along with the seeds.

- DAP is the second most-used fertiliser in India, with average yearly sales of 103.4 lakh tonnes over the past five years—second only to urea, which has average sales of 359 lakh tonnes.

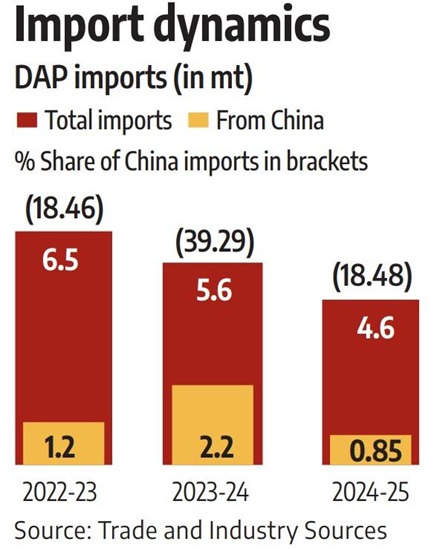

- India imported around 4.6 million tonnes of DAP in FY25, according to industry sources. Chinese imports were 0.85 million tonnes, or 18.4 per cent, of that amount.

- Moreover, India also imports phosphorus and ammonia needed for manufacturing DAP.

- A $10 per tonne increase in the price of imported phosphorus leads to almost $5 per tonne rise in finished DAP rates.

- A $30 per tonne increase in ammonia prices leads to $12 per tonne rise in finished DAP rates.

Opportunity for India

- Due to China’s export restrictions, DAP sales in India dropped from 108.1 lt in 2023–24 to 92.8 in 2024–25, with further decline in April–May.

- Experts see this as a positive shift, encouraging balanced fertilisation over high-analysis fertilisers like DAP or urea.

- Sales of NPKS complexes rose by 28.4%, with APS (20:20:0:13) emerging as the third most-used fertiliser due to its balanced N-P ratio and sulphur content.

- Companies like Coromandel and IFFCO are promoting it actively. Single Super Phosphate (SSP) use also rose, offering a cost-effective, sulphur-rich alternative.

- This shift may help improve soil health and reduce dependency on imports.

New Market Dynamics of DAP

- In recent years, DAP has been treated almost like a price-controlled fertiliser, similar to urea.

- The Central government has unofficially set its retail price at ₹1,350 for a 50-kg bag. However, farmers often end up paying around ₹1,700.

- In comparison, Ammonium Phosphate Sulphate (APS) sells for ₹1,350–1,400, and other NPKS complex fertilisers like 10:26:26:0 and 12:32:16:0 cost ₹1,700–1,800 per bag.

- In the long run, limiting DAP use may not be a bad idea since India has very little rock phosphate of its own.

- So, it must either import DAP directly or produce it using imported phosphoric acid or rock phosphate.

- By reducing or capping DAP consumption, India can use these imported materials more efficiently and save valuable foreign exchange.

Mains Practise question

In light of the recent decline in DAP availability due to China’s export restrictions, examine how this disruption has influenced fertiliser usage patterns in India. Can this shift towards balanced fertilisers like APS and SSP lead to more sustainable agriculture? (15M, 250W)