Context:

Recently, the Pradhan Mantri Kisan Maandhan Yojana (PM-KMY) completed five successful years since its introduction in 2019.

Pradhan Mantri Kisan Maandhan Yojana (PM-KMY)

- PM-KMY was launched for providing social security to all eligible Small and Marginal Farmers (SMFs) across the country by providing a fixed monthly pension of 3000/- rupees after attaining the age of sixty.

- Marginal farmers are those holding below 1.0 hectares of cultivable land and, farmer holding 1.0 to 2.0 hectares of land are termed as small farmers.

- It is a Central Sector Scheme, administered by the Department of Agriculture, Cooperation & Farmers Welfare, Ministry of Agriculture & Farmers’ Welfare, Government of India in partnership with the Life Insurance Corporation of India (LIC).

- This old-age pension scheme is a voluntary and contributory pension scheme.

- Scheme enrolment: SMFs can be enrolled by paying a monthly subscription to the Pension Fund. Farmers aged between 18 and 40 years need to contribute between Rs. 55 to Rs. 200 per month until the age of 60.

- The Life Insurance Corporation (LIC) manages the pension fund, and beneficiary registration is facilitated through Common Service Centres (CSCs) and State Governments.

- Common Services Centres are the access points for the delivery of Government-to-Citizen (G2C) e-Services within the reach of the citizen, by creating the physical service delivery Information and Communication Technologies (ICT) infrastructure.

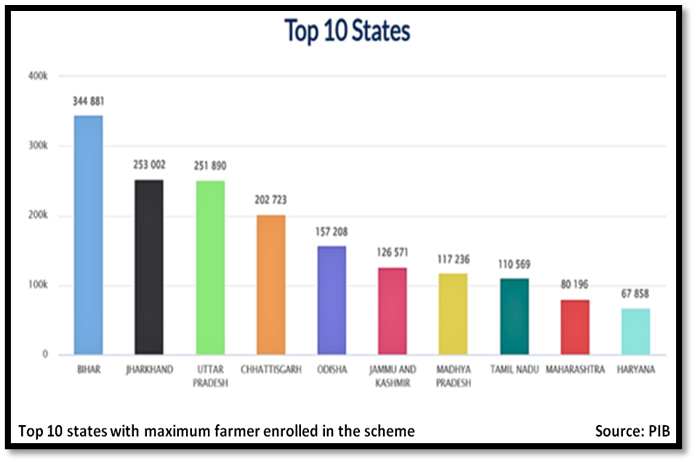

- As of August 6, 2024, a total of 23.38 lakh farmers have joined the scheme. Bihar is the leading state with over 3.4 lakh registrations followed by Jharkhand with over 2.5 lakh registrations.

- The State / UT Governments have the option of sharing the burden of individual SMF beneficiary’s contribution.

Key Benefits Under (PM-KMY)

- Family Pension: If a subscriber passes away while receiving their pension, their spouse will be entitled to a family pension equal to 50% of the amount the subscriber was receiving i.e. Rs.1500 per month as Family Pension. This is only applicable if the spouse is not already a beneficiary of the scheme. The family pension benefit is exclusively for the spouse.

- PM-KISAN Benefit: SMFs can choose to use their PM-KISAN benefits to make voluntary contributions to the scheme. This will authorize automatic debit of their contributions from the bank account where their PM-KISAN benefits are credited.

- Equal Contribution by Government: The Central Government, through the Department of Agriculture Cooperation and Farmers Welfare, also contributes an equal amount as contributed by the eligible subscriber to the pension Fund.

Leaving the Pension Scheme

- If an eligible subscriber exits the Scheme within less than ten years of joining, then the share of contribution will be returned along with the savings bank rate of interest payable thereon.

- If the subscriber exists after ten years but before attaining sixty years of age, they will receive their contribution plus accumulated interest, either as earned by the Pension Fund or at the savings bank rate, whichever is higher.

Significance of the Scheme

- PM-KMY has significantly empowered Small and Marginal Farmers (SMFs) by providing financial stability amidst the uncertainties of seasonal agriculture and fluctuating incomes.

Shortcomings of the Scheme

- Eligibility: The scheme is for farmers owning up to two hectares of cultivable land, excluding tenant farmers, sharecroppers, and larger landowners.

- Contribution: Farmers must contribute monthly, which can be a burden for those with irregular incomes.

- Implementation: Reports indicate delays in enrolment and issues with the auto-debit system for contributions.