SYLLABUS

GS 3: Indian Economy and issues relating to planning, mobilization of resources, growth, development and employment; Changes in industrial policy and their effects on industrial growth; Investment models.

Context: Recently, the Centre notified the conditional customs duty concessions on clearance of goods manufactured in Special Economic Zones (SEZs) to the Domestic Tariff Area (DTA) to improve capacity utilisation of manufacturing units impacted by global trade disruptions.

More on the News

• It will benefit approximately 1,200 SEZ manufacturing units by enabling economies of scale, reducing costs and enhancing resilience, while preserving the export-oriented nature of SEZs.

• Duration: The notification is effective from April 1, 2026, to March 31, 2027.

• Concessional Rates: Eligible SEZ manufacturing units are permitted to supply goods to the DTA at concessional duty rates, up to 30% of the highest FOB export value achieved in any of the three preceding financial years.

- To prevent double benefits, export incentives such as duty drawback on inputs are not permitted on such withdrawals.

- The DTA refers to the entire country of India (including the territorial waters and continental shelf) but excludes the specific designated areas of SEZs.

- As per Section 30 of the Special Economic Zones Act, 2005, clearance of goods from SEZs to the DTA is treated as imports into India and attracts applicable customs duties.

• Eligibility: The notification sets key eligibility criteria, including a minimum 20% value addition within the SEZ, calculated through a specified formula based on assessable value and input costs.

• Wide Sectoral Coverage: The concessional framework spans a wide range of sectors, including minerals, chemicals, plastics, leather, wood and paper, textiles, footwear, ceramics and glass, metals, machinery, transport equipment, instruments, arms, and other manufactured goods.

- However, sectors such as agriculture (including marine and processed food products, tobacco, etc.), marble and granite, gems and jewellery, vehicles, toys and petroleum are excluded.

• Compliance Requirements for Concessional Duty: To avail concessional duty benefits, SEZ units must submit a certificate from the Development Commissioner confirming compliance, along with an undertaking to pay full duty in case of non-fulfilment.

• Audit: The units will also be subject to audit under the SEZ Rules, 2006.

About Special Economic Zones in India

• A Special Economic Zone (SEZ) is a specifically delineated duty-free enclave treated as outside India’s customs territory for authorised operations. It operates under a distinct regulatory and fiscal framework to promote trade and investment.

• SEZ units are set up for manufacturing, providing services, and undertaking warehousing activities, including through Free Trade Warehousing Zones.

• Objectives of SEZs: SEZs serve as engines of export-led growth by generating additional economic activity, boosting exports, attracting domestic and foreign investment, creating employment opportunities, and developing world-class infrastructure.

• Currently, there are 368 notified SEZs across India as of 28th February, 2026.

Key Incentives & Facilities Offered to the Units in SEZs

• Duty-free import/domestic procurement of goods for development, operation and maintenance of SEZ units.

• Exemption from Central Sales Tax, Service Tax and State Sales Tax. These have now been subsumed into GST, and supplies to SEZs are zero-rated under the IGST Act, 2017.

• Other levies, if exempted by the respective State Governments.

• Single window clearance for Central and State-level approvals.

Special Economic Zones Act, 2005 and Special Economic Zones Rules, 2006

• The SEZ Act, 2005, along with the SEZ Rules, 2006, introduce a simplified framework with single-window clearances for Central and State approvals.

• The Act sets out guiding principles for SEZs—promoting economic activity, infrastructure development, and employment generation—while also mandating environmental compliance by developers and units.

• The performance and impact of SEZs under the framework of the SEZ Act and Rules, with the Government evaluating outcomes based on monthly reports submitted by Development Commissioners, who are appointed by the Government to oversee the functioning, approval, and compliance of SEZ units.

• SEZ Rules, 2006 were amended in June 2025 to facilitate the establishment of SEZs exclusively for the manufacturing of semiconductors and electronic components.

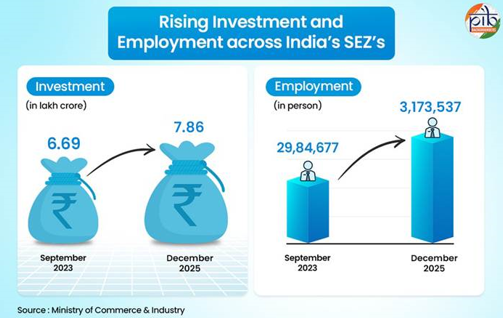

India’s SEZ Performance Snapshot

Key Concerns Before SEZs

• Declining Export Competitiveness: SEZs face pressure from global trade disruptions, rising protectionism, and competition from countries like Vietnam and Bangladesh, affecting export performance.

• Underutilisation of Capacity: Many SEZ units operate below capacity due to subdued global demand and limited domestic market access.

• Erosion of Fiscal Incentives: Gradual phasing out of tax holidays and incentives has made SEZs less attractive compared to earlier years.

• Infrastructure and Logistics Bottlenecks: Inadequate connectivity, high logistics costs, and delays in infrastructure development affect efficiency.

• Land Acquisition and Social Concerns: Issues related to land acquisition, rehabilitation, and environmental clearances create delays and resistance.

• Policy Uncertainty and Frequent Changes: Frequent amendments in tax regimes (e.g., transition to GST, withdrawal of certain exemptions) have reduced predictability for investors.

SOURCES

PIB

Tribune India

PIB