SYLLABUS

GS 3: Indian Economy and issues relating to planning, mobilization of resources, growth, development and employment.

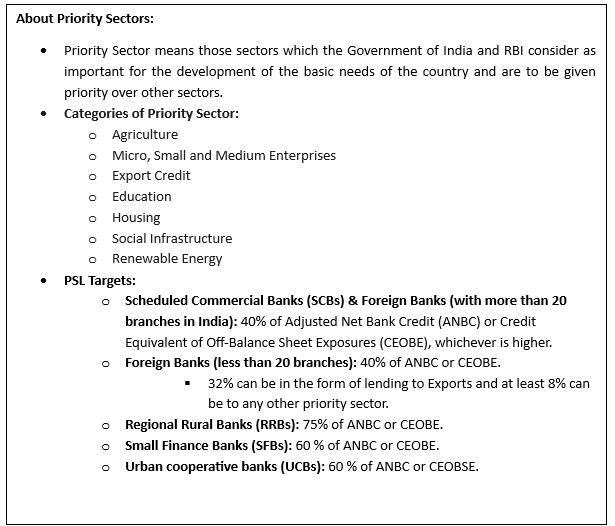

Context: The Reserve Bank of India (RBI) has introduced stricter PSL compliance norms, making external auditor certificates mandatory to avoid duplication of loan claims.

More on the News:

- The new directive follows the RBI’s amendment to the ‘directions on priority sector lending – targets and classification ‘ issued on 19 January 2026.

- This move comes after HDFC Bank and ICICI Bank reported that the regulator has found mismatches in their PSL classification of Agri loans.

Provisions of New Compliance Framework

- External Auditor Certification: all intermediary lenders including microfinance institutions, non-banking finance and housing finance companies to submit external auditor certificates confirming that no loan is claimed as priority sector by more than one bank.

- PSL classification for the loan: Lenders can claim PSL classification for loans extended to NBFCs (Non-Banking Financial Company), provided that the assets financed through these loans qualify as PSL-eligible assets.

- Loans extended by banks to microfinance institutions (MFIs) can be classified as PSL under relevant categories such as agriculture, MSME, social infrastructure, provided the MFIs comply with RBI guidelines.

- Bank credit to housing finance companies for the purpose of purchase/construction/ reconstruction of individual dwelling units or for rehabilitation of slum dwellers, will also be eligible for PSL classification subject to Rs 20 lakh per borrower limit.

- Bank lending will be capped at 5 % of a bank’s total PSL of the previous financial year for NBFC and 10% for NBFC-MFIs.

- Export credit included in PSL: Export credit for agricultural and MSME sectors can be counted under PSL loan by banks, subject to category-wise aggregate limits.

- NCDC Credit Eligible for PSL: Lending to the National Cooperative Development Corporation (NCDC) will qualify as priority sector loans, aiming to expand credit to cooperative societies

- Co-lending provisions: Banks are also permitted to enter into co-lending arrangements to meet PSL targets.

- Co-lending refers to the collaborative loan service where two lending institutions jointly fund loans to borrowers.

- Strengthened Oversight: Banks will be required to furnish PSL data at quarterly and annual intervals within 15 days and one month respectively from the end of the reporting period.

- Exclusion of service charges: RBI banned service charges on priority sector loans up to Rs 50,000, with the limit applicable per member in the case of SHGs.

- PSL computation framework: The credit equivalent of off-balance sheet exposures will be calculated in line with the large exposures Framework and the applicable capital adequacy directions.

- As per large exposure framework, a bank’s total exposure to a single borrower cannot exceed 20 % of its eligible capital base (Tier 1 capital), and 25 % in the case of corporate group.