SYLLABUS

GS-2: Government Policies and Interventions for Development in various sectors and Issues arising out of their Design and Implementation.

GS-3: Indian Economy and issues relating to Planning, Mobilization of Resources, Growth, Development and Employment.

Context: The recent World Bank’s State and Trends of Carbon Pricing 2025 report highlights that carbon markets across the world are expanding at an unprecedented scale.

Key findings of the Report

- Booming of Carbon Market: Global revenues from carbon taxes and emissions trading systems crossed $100 billion for the second consecutive year.

- A carbon market is a market-based mechanism that puts a price on carbon emissions, allowing entities to buy and sell emission permits or carbon credits to reduce greenhouse gas (GHG) emissions cost-effectively.

- Growing acceptance of carbon pricing: Nearly 28 per cent of global greenhouse gas (GHG) emissions are now covered by a direct carbon price, compared to just 5 per cent in 2005.

- 80 direct carbon pricing instruments operating worldwide, including 37 emissions trading systems and 43 carbon taxes.

- Carbon pricing being used as a fiscal instrument: In 2024, 56% of global carbon pricing revenues were directed towards environmental programmes, infrastructure and development spending.

- Supply Outstrips Demand: The supply of carbon credits continued to outpace demand, leaving nearly 1 billion tonnes of unretired credits in global markets.

- Key Challenges:

- Ground Realities: Rising revenues and wider coverage do not automatically translate into deep emission reductions.

- Less certainty on Absolute emission reductions: Many emerging economies, including India, have adopted rate-based emissions trading systems, which regulate emissions per unit of output rather than imposing an absolute cap on total emissions.

- India-specific findings:

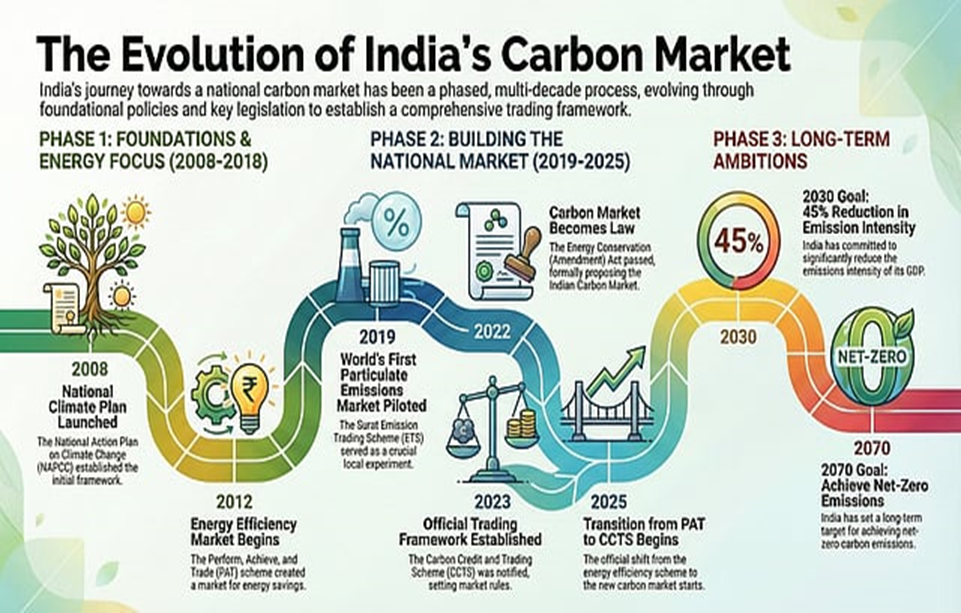

- India’s carbon market: The Carbon Credit Trading Scheme (CCTS) initially covers nine energy-intensive industrial sectors and is intended to help India meet its commitment to reduce the emissions intensity of GDP by 45 per cent by 2030.

- Legacy of Perform, Achieve and Trade (PAT): Targets under PAT were generally modest, allowing many industries to not only easily comply but also overachieve without significant technological upgrades.

- Sectoral coverage gaps: Many key sectors such as agriculture and waste remain outside carbon pricing.

- Gaps in CCTS: Evidence from India’s earlier market-based programmes suggests that weak targets, limited sectoral coverage and poor governance can significantly dilute climate outcomes.

- Poor Compliance: Surplus of energy-saving certificates, particularly during PAT Cycle II, when more than two million excess certificates entered the market. Prices collapsed, making compliance cheaper than investing in cleaner technologies

- Thermal power sector, despite being India’s largest source of emissions (40 per cent), cumulative carbon dioxide emission reductions achieved under PAT over six years were less than 2.5 per cent of emissions in a single year (2016).