Context: India’s Income Tax Bill, 2025, recently introduced a legal framework for Virtual Digital Assets (VDAs).

- Virtual Digital assets (crypto assets) refer to any digital representation of value that can be digitally traded, transferred, or used for payment.

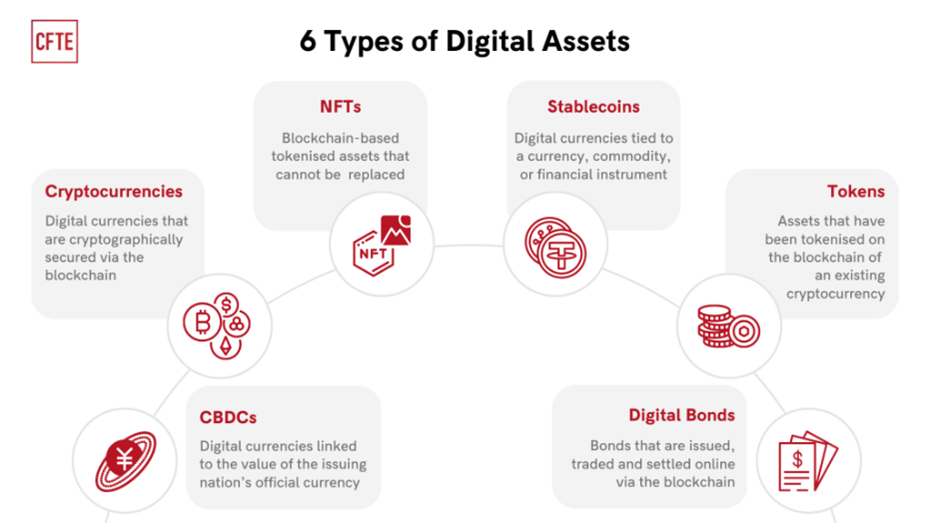

- It is found in the Income Tax Bill, 2025 Section 2(111) and Section 92 (5)(f) and includes digital assets like cryptocurrency and Non-Fungible Tokens (NFTs).

- India’s bill treats VDAs (including cryptocurrencies and NFTs) as property and capital assets for the first time.

- The government ensures they are taxed under standard asset principles, preventing misuse as unregulated financial instruments by classifying VDAs as capital assets.

- India has now aligned with countries like the U.K., the U.S., Singapore, and Australia to treat VDAs as property or securities.

Implication of VDA

- VDAs are classified as capital assets under Section 76(1).

- By treating VDAs as capital assets, any gains from their sale, transfer, or exchange are subject to capital gains tax, similarly as stocks or real estate transactions are taxed.

Taxation on VDAs

- The Bill introduces a 30% tax on income generated from the transfer of VDAs.

- Flat tax rate with no deductions allowed, except for the acquisition cost.

- Transaction fees, mining costs, and platform commissions cannot be deducted while calculating taxable income.

- 1% Tax Deducted at Source (TDS) on VDA transfers under Section 393, even for peer-to-peer (P2P) transactions.

- The threshold for TDS exemption is ₹50,000 for small traders and ₹10,000 for others.

Reporting and Enforcement Measures

- Undisclosed Income: Under Section 301, failure to report VDA holdings in tax filings will lead to these assets being treated as undisclosed income and taxed accordingly.

- Seizure of VDAs: Section 524(1) grants tax authorities the power to seize VDAs during investigations or tax raids, just like cash, gold, or real estate.

- Transaction Reporting: Section 509 mandates that all entities dealing in crypto assets, including exchanges and wallet providers, report transactions in a prescribed format.

- Ensures transparency and makes it difficult to launder money through digital assets.

- VDAs must be included in Annual Information Statements (AIS), automatically recording crypto transactions in taxpayers’ financial profiles.

Challenges and Future Outlook

- While the changes in classification and taxation are significant, India’s regulatory framework still faces challenges.

- There is a lack of comprehensive guidelines covering areas like:

- Investor protection

- Market regulation

- Enforcement mechanisms

- Consumer rights